With agricultural commodities prices falling and the prospect of rising interest rates getting closer, I thought it could be interesting to see where the Canadian agriculture stands debt-wise. In this post, I will look at the indebtedness in two ways.

Firstly, farm indebtedness will be assessed relative to the output of the Canadian agriculture. We start by deflating the farm debt value by the CPI. The output is derived from the value of the production (farm sales and change in inventories) by deflating it by the farm products price index. By building an index, we are able to obtain the change in our ratio [Farm debt / Output].

We do the same with the Gross value added (GVA) of the Canadian agriculture and the total value of farm assets (real estate and quota).

The first graph below presents the evolution of our three ratios. What really stands out is:

- the significant decrease of the economic efficiency (GVA/Output) of the Canadian agriculture over the period considered here (1981-2014) though it has bounced back a bit over the last 10 years thanks to high prices.

- from 1995, the divergence of dynamics between, on one hand indebtedness and farm assets value, and on the other economic efficiency.

That could be explained mainly by two factors :

- lower interest rates which are now close to the lowest level they could reasonably be at;

- the increasing share of off-farm income in the farm households which is not captured by the GVA account, and that provides liquidity to repay debt obligations

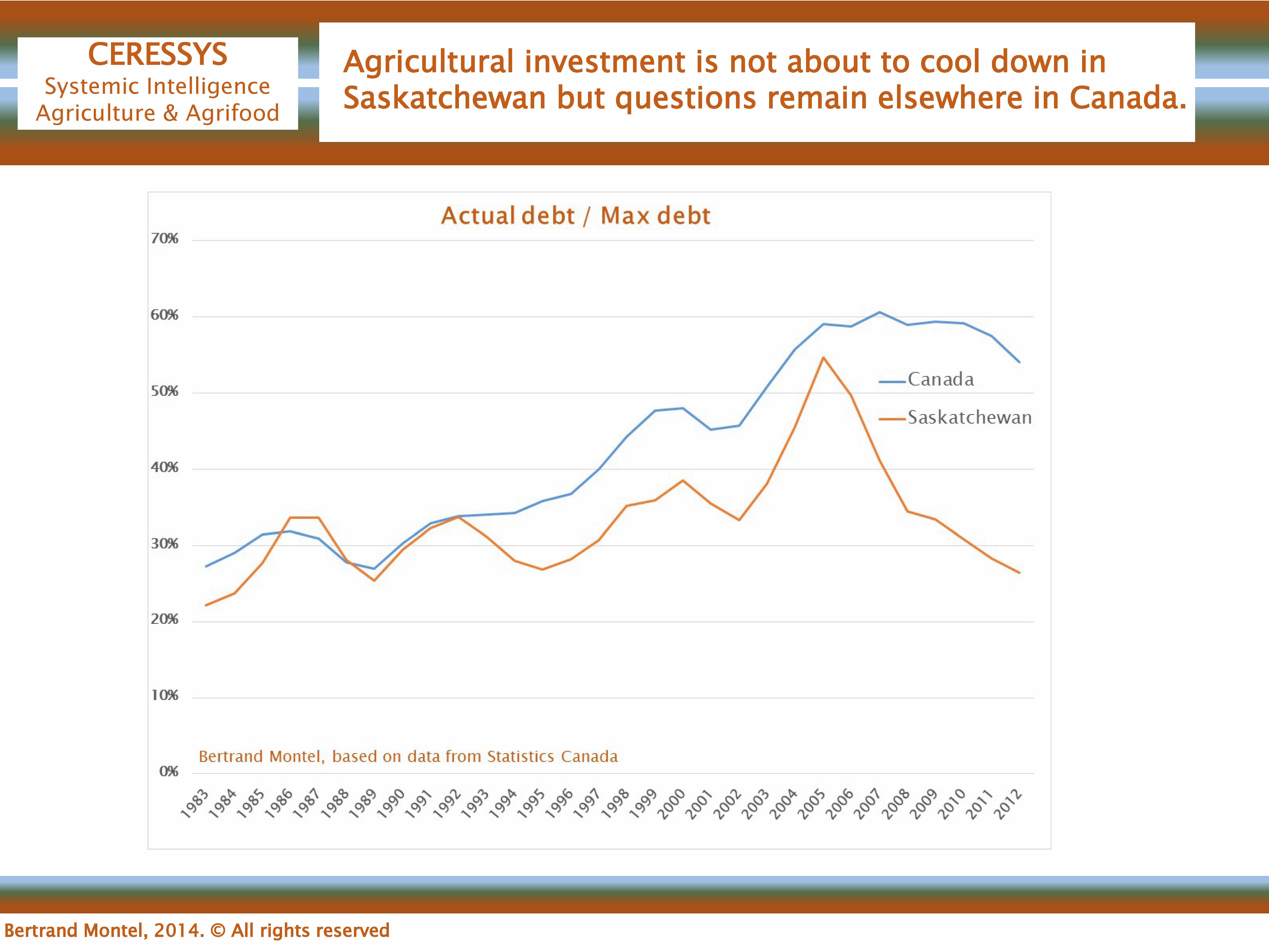

Secondly, we will look at the indebtedness in the Canadian agriculture through the ratio (Farm debt outstanding)/(Maximum farm debt).

Maximum farm debt is defined as the long-term debt allowed by the aggregate debt servicing capacity, assuming terms and conditions complying with current best agricultural lending practices:

- Debt service coverage ratio of 1.1, calculated as Earnings before Interest, taxes, Depreciation and Amortization (EBITDA) divided by Principal plus Interest payment. Using Statistics Canada data, EBITDA is approximated by Net cash income plus interest. Because of the intrinsic volatility of farm income, we will use a 3-year average of net cash income before interest in place of the current value to calculate our debt repayment capacity.

- Repayment period based on useful life of assets. Usually, it is based on the weighted average of the useful life of the different asset classes. However, in order to assess the maximum level of debt, we could use a 20-year repayment period providing the ratio Maximum debt to total Land value remains below 75%. If that ratio was to be above 75%, we would have to revert to the weighted average, with 15 years a good benchmark.

- Prudent interest rate: the 5-year conventional mortgage rate which is commonly used to stress-test credit risk of agricultural loans. Comparing it to the apparent average interest rate paid by farms, we could note that from the mid-90’s, the spread between the two interest rates is relatively stable.

The graph below shows that indebtedness capacity became more and more saturated until 2005-2007. Then, lower interest rates, increasing farm products and farmland prices, all contributed to raising the maximum farm debt.

We note that two provinces stand out : Saskatchewan and British Columbia (BC). The former has experienced a remarkable drop in indebtedness saturation because all the recent trends mentioned previously were amplified here. The latter, a contrario, has experienced a very significant jump with a current indebtedness saturation of more than 100%. How is that possible? Short answer: off-farm income, low interest rate, non-standard lending term and conditions, farmland prices driven by non-agricultural factors.

Now, we will assume that the interest rate gradually reverses to its 20-year mean over 10 years while debt repayment capacity, farm debt and land value remain constant. That sole change would lead to increasing saturation of the indebtedness capacity. However, we could construct realistic scenarios which would lead to a much faster saturation.

As far as I am concerned, the debt problem of the Canadian agriculture is not a problem of solvency. The Canadian agriculture is solvent. I do not foresee any collapse of crisis-scale within the next decade. It is a problem of restricting the ability of the Canadian agriculture to sustain, over the long term, a level of investment consistent with the competitive pressure, the pace of innovation and of demographic change.

Then, questions come to mind: Why debt? Are there other sources of capital available?

This is a first-level analysis at a very aggregated level. To assess the risk identified here adequately, we need to dig deeper and go to disaggregated levels. Preliminary results show differences along industry and farm-size lines.