The current debate about the TPP negotiations and their consequences for the future of supply management in Canada is not about the merits and benefits of supply management themselves. It is about Canada’s bargaining power in negotiations it has been invited to and to which it may not be an essential party. As of now, it seems that Canada has a rather weak hand and will have to commit to open its dairy market somehow or risk being sidelined. I’m not privy to the negotiations and my opinion has been forged on what has been publicly disclosed.

Supply management has undeniably served the Canadian dairy industry very well, allowing among other thing dairy farmers to increase their income and wealth over the years and two dairy processors (Saputo and Agropur) to develop into major global players. Over the period 1998-2014, the number of dairy farms has been almost halved. Production has increased only by 4%, following a sleepy growth in consumption of dairy products driven by demographics and changes in food consumption pattern. Today, the three largest dairy processors control about 80% of the market. The Canadian dairy industry could be said to be relatively mature. However, even if supply management survives the current TPP negotiations, its future is uncertain as adverse forces are gathering strength, threatening the three pillars of supply management (import control, producer pricing and production discipline) from within.

The strongest force is the weakness of growth potential in the domestic market which, because of supply management, will translate into a marginal production increase. On the processing side, maintaining or increasing margin will then require to lower supply cost, which will result in a downward pressure on milk price and concomitantly in an increased use of imported ingredients which in turn will reinforce the former. In the meantime, and considering productivity gains and labour shortage in dairy production, there will be tremendous pressure to realize some economies of scale at the farm level to limit the ongoing deterioration of profitability in many dairy farms. Even so, more voices getting louder may call for increasing market potential by making it possible to export Canadian dairy products, which would antagonize import control.

Now the second significant force, quota mobility. Pressure to further consolidation at the farm level will certainly build up as previously shown. This will require that quota is made available for purchase. However, the quota exchange market has become rather illiquid over the last seven years or so. This change has been most remarkable in Ontario and Quebec after new regulations of quota exchange were introduced in 2007. A trigger is needed to incentivize the sale of quota. Will it be sufficient to decrease milk price? Shall we lower the existing price cap? Shall we let the price be set freely? Shall quota move unhindered between province? All this in a context where there are expectations to maintain as many dairy farms as possible in as many regions as possible. Quite a catch 22, isn’t it. Some unruly producers may end up challenging production discipline.

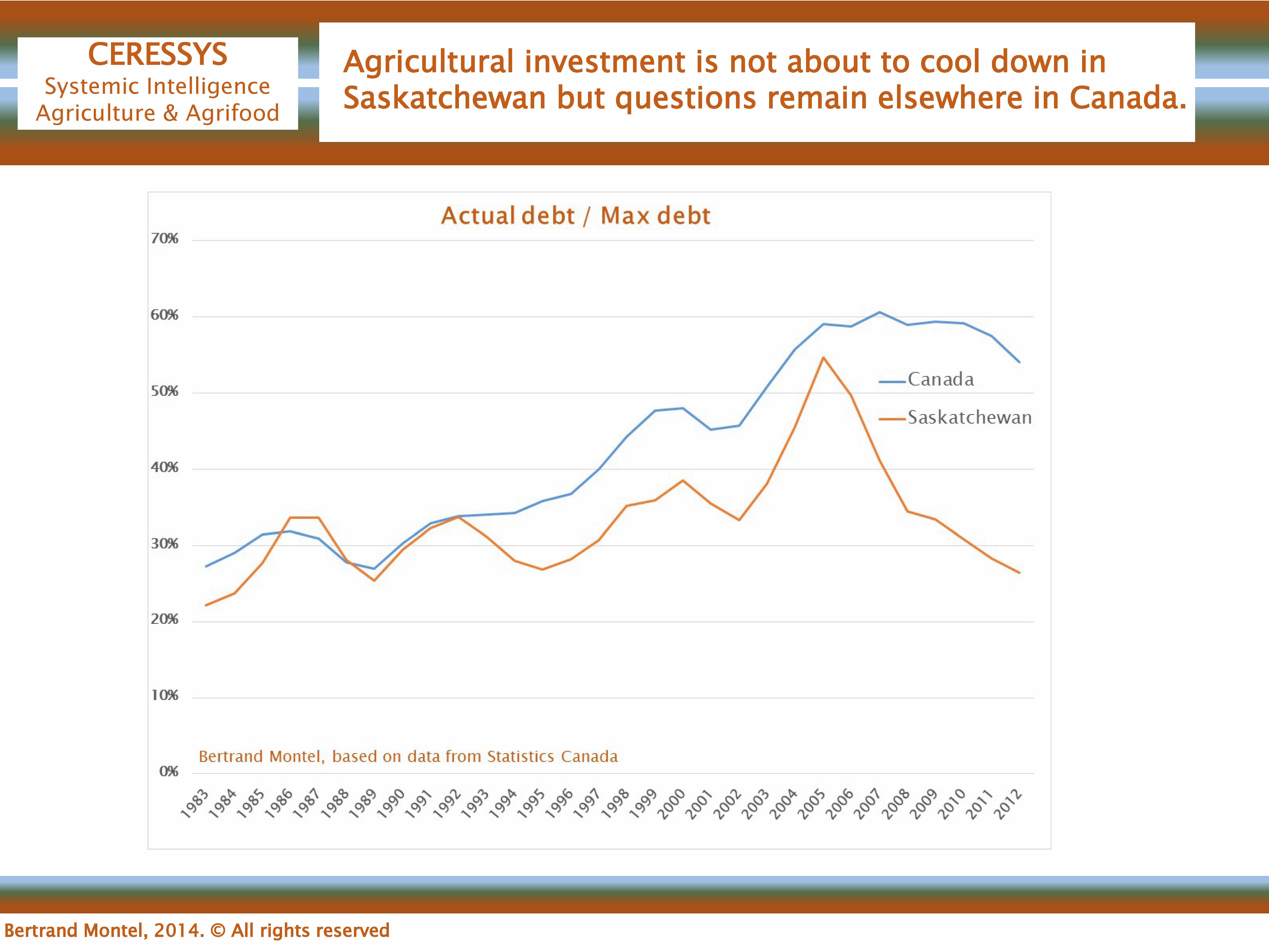

The third force is indebtedness arising from the cost of capital which in turn stems from the price of quota. Indeed, one must not forget that acquiring quota is just the first step but a costly one. Additional investments (buildings, equipment, farmland, herd genetics, etc.) are needed to maintain consistent dairy production systems. This will be especially critical in Quebec where almost all dairy barns are of the tied-stall type, which is ill-fitted for the automation of milk production processes. Besides, these barns are ageing, which combined with work overload could make it more difficult to maintain good herd health status and consistent milk quality, both being key to the farms’ competitiveness. Consequently, heavy investments will have to be made over the next ten to fifteen years in order to achieve a full-scale modernization of Quebec dairy production. Meanwhile, the sources of capital available to the Canadian agriculture are essentially restricted to debt. Already indebted farms will thus have to carry on more debt, pressuring their profitability further. Quebec dairy farms will be particularly exposed to that risk. Here, it is worth remembering that, for instance, if the current dairy crisis in New Zealand has indeed been triggered by a sudden drop in price, one of the main structural fault lines has been excessive indebtedness. So, the very economic sustainability of many dairy farms will hinge on higher milk price while the most efficient ones may still prosper in this lower-price environment. Consequently, producer pricing will become even more conflictual as increasingly diverging interests are expressed along the value chain and within different groups of stakeholders.

These conflicting dynamics may give enough strength to centrifugal forces, make one of the, or all three pillars of supply management crumble. Quebec may well be at the epicenter of this quake.

This is why I think the phasing out of supply management will be initiated before 2030, regardless of any trade negotiations.

Supply management as such is a sound policy. However, it cannot pretend to remain unquestionably relevant forever. This is why I think it is time to engage in a comprehensive review of supply management, followed by an open debate over its future, over the why and how of supply management.